No doubt you will come across these two methods of investing your money and may be asking yourself, which one is best? Some investors strictly lump sum invest, whilst others claim regular saving is the most sensible way to invest as a start. Needless to say, either option is better than not investing at all — trying to time the market just doesn’t really pay off.

First off, I am a fan of each method, choosing to invest with both strategies for my long-term savings goal. Others strictly lump sum invest and will argue just for that — each to their own. Let’s take a look at both the strategies before assessing how these methods can work together to create a solid long-term savings portfolio.

Regular Savings

Stashing away a portion of your salary each month is a solid foundation for your long-term savings. Even better is when you invest that money, rather than simply deposit it in a low-interest bank account — mix that with high inflation and your long-term savings aren’t making its worth.

Investing this way benefits from “dollar-cost averaging”. Rather than invest a lump sum, you contribute a regular, monthly amount into an investment regardless of market conditions and continue to do so over the long-term, say 15 years or more. This is often called “drip feeding” into the markets.

Locking this money away yields the benefit of compound interest in the long run — your best friend when it comes to investments — as the “interest on interest” spikes into high returns over time. Even Einstein marvelled its significance!

Dollar-cost averaging isn’t glamorous and doesn’t seek grand returns — yet it is a fantastic long-term savings plan and a brilliant start towards your investments. Let’s take a look at why.

Reduces Risk

Investing like this takes away the element of market timing, meaning you consistently buy no matter a low or high environment.

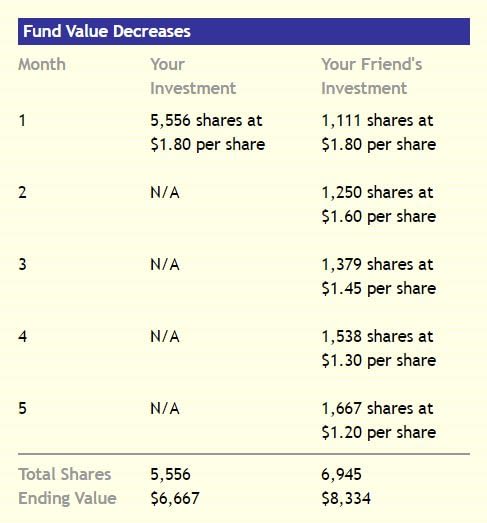

Notably, it can also help reduce the losses in a declining market, as seen below.

Here, you and your friend make a loss — but your friend makes less losses by averaging. On a further positive, when the market rebounds they will own more shares and realise more gains.

Discipline

Investors are notorious for buying high and selling low, driven by their emotions and market “noise“, paying the price for trying to time the market (which rarely pays off). Dollar-cost averaging takes away market timing by consistently contributing, no matter the conditions. Better yet, setting up an automatic investment of this kind creates a simple yet effective “set and forget” strategy, keeping you saving each month without too much thought.

Quality Funds

I’m an advocate of passive investing and work a lot with ETFs on my lump sum investments, but there’s no denying the effectiveness of mutual funds — no more so than when it comes to dollar-cost average saving, where monthly trading with ETFs can incur significant trading costs.

The reason for this is that many mutual fund companies waive their initial minimum investment to investors who set up a regular investment plan, granting the beginner investor easy access to high-quality, otherwise inaccessible funds, with as little as a couple of hundred dollars a month.

Lump Sum Investing

Putting all your money to work at once is a preferred option by many investors; considering that the markets tend to go up more than they do down, this is generally a higher-yielding strategy versus dollar-cost averaging, over the long-term.

However, it is important to realise that losses are bigger along the way with lump sums, yet the overall gains outweighs the same investment by dollar-cost averaging.

Research from Vanguard evidenced that for most of the time lump sum investing trumps dollar-cost averaging, owing to the fact that markets are up roughly three out of every four years. This strategy wins about two thirds of the time.

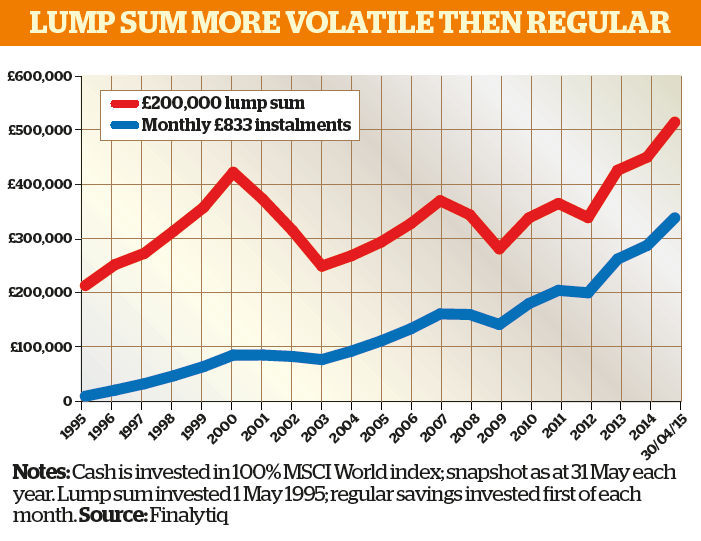

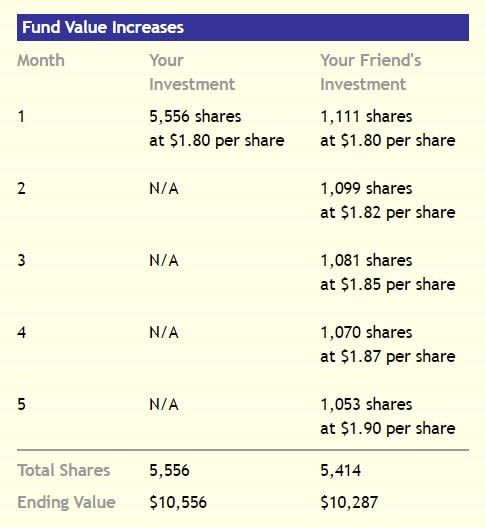

Here’s how $10,000 invested all-in would work against “drip feeding” $2000 a month, over a 5 month period:

We have seen that dollar-cost averaging helps diminish our losses when the markets slump, yet lump sum investing achieves greater long-term results due to markets generally going up, as history has shown.

Turn successively positive months into years and your lump sum investment will yield greater results over the long run, as seen in the history of the markets.

So, What’s Best?

There’s no “best” method here — it’s up to your preference. As long as you are doing something and the earlier the better.

It is easy to think that lump sum investing provides greater returns over the long-term, so why not just invest this way? I wouldn’t argue that statistics show it is generally the case, but it’s important to understand why that is so, i.e. accepting higher losses along the way and being able to ride out the negative periods. Yet, dollar-cost averaging also has its benefits in times of market downturns.

Let’s sum up both methods:

“Investing all of your cash at once gives you a higher probability of taking part in larger gains but also taking part in larger losses. To decrease market risk and sleep better at night, dollar cost averaging in a higher valuation environment can lead to a smoother ride and give a lower probability of seeing large losses. ” (Bloomberg)

So, why do I prefer benefitting from dollar-cost averaging and lump sum investing? Why not just invest in one strategy? Simply put, because combining the two creates a solid, twofold plan for your savings: disciplined and strategic.

For me, smaller monthly amounts in a regular plan is my less volatile, disciplined form of savings — the bulk of my excess money is invested as a lump sum, where I am more aggressive in order achieve higher returns over the long run. I understand I may make losses along the way, but at least I have a regular plan in place smoothly amassing wealth for my future thanks to dollar-cost averaging.

A regular plan is a savings scheme focused on a dominant long-term goal, which doesn’t regard what is going on in the financial markets, slowly but surely building a considerable wealth for your future. This can be an affordable couple of hundred dollars a month that you “set and forget”, allowing you to focus excess savings towards your lump sum investments, knowing you have a plan ticking over in the background.

With a lump sum plan we still hold a long-term view, but by working with a higher amount we benefit from the markets generally going up, allowing the lump sum investment to realise greater gains than our regular savings over the same time.

Both require consistent management to keep things in check, although a regular plan can be left to carry on quite systematically whilst you may increase the monthly contributions when you earn more. With your lump sum portfolio, extra top ups are normally added in larger chunks when you have excess savings, injecting more money to work rather than dripping it in.

In summary:

Regular Savings — smaller amounts consistently

Lump Sum Investing — larger amounts, top up with extra “lumps”

My advice? Combine the two! Set up a regular plan with a smaller amount from your salary and then invest with lump sums from excess savings — either way, money invested is better than left sitting stagnant and losing value.

Just don’t put it under your mattress.

Of course, you can choose whatever style fits you best — but if you haven’t got anything set in place and want some advice, drop me an email at thomas(at)absolutefsl.com to see how I can help you out.