You’re young and you may be feeling financially lost…if you aren’t — good on you! Managing your personal finances can seem overwhelming, between paying rent, student debt and just general “life” stuff. I mean, when did they teach us about this growing up? Here’s my Top 3 plan on how you can start now — without the help of a financial advisor — to help you get on your way in the big, bad scary world out there.

During an A Level maths class, I asked the teacher when the algorithm we were learning may be used in the real world. She racked her brains, before supposing that it may be used by a plumber. I then dared to ask if ‘said’ plumber could just use a calculator…you can guess the answer.

The point of this little anecdote is that whilst I learned and can remember how to work out things like the hypotenuse of the triangle, entering the adult world I have never used this theorem. Instead, I was ill-prepared when I had to face taxes, budgeting, savings and generally anything to do with personal finances. Financial education is rather lacking, but that’s content for another time.

Now, I’m sure most of you know the benefits of saving, but aren’t quite sure what best to do with that hard-earned cash, besides spending it on holidays and down at the pub. Work-life balance is crucial, but if like most people your end goal is retirement, then starting to organise your personal finances early really is better in the long run.

Let’s look at three simple places where we can start.

Budgeting

Ideally, we’d all be bringing back enough bacon to spend what we want and not have to worry about our spending. Wouldn’t that be great? But, for most of us in our 20s, we’re not quite there yet. Budgeting makes me cringe, but it shouldn’t have to be too terrifying to manage if you make a plan to follow.

One thing I do is keep a track of my expenditure over the month. There are many great apps out there for this; I personally use Monefy, where I input any expense each day into their respective category, cleanly visualising where I am spending with clear percentages against my income. Now, I’ll be honest – whilst I can clearly see where I am spending my money, it doesn’t always stop me from “just one more” when out for a drink, for example. The app sure helps me feel guilty about any unnecessary expenditure and highlights areas where I can be more frugal, but discipline does come into play. It has helped me to stop overbuying sugarless dark chocolate, for example – just because it’s “healthier” doesn’t mean I need it once a week!

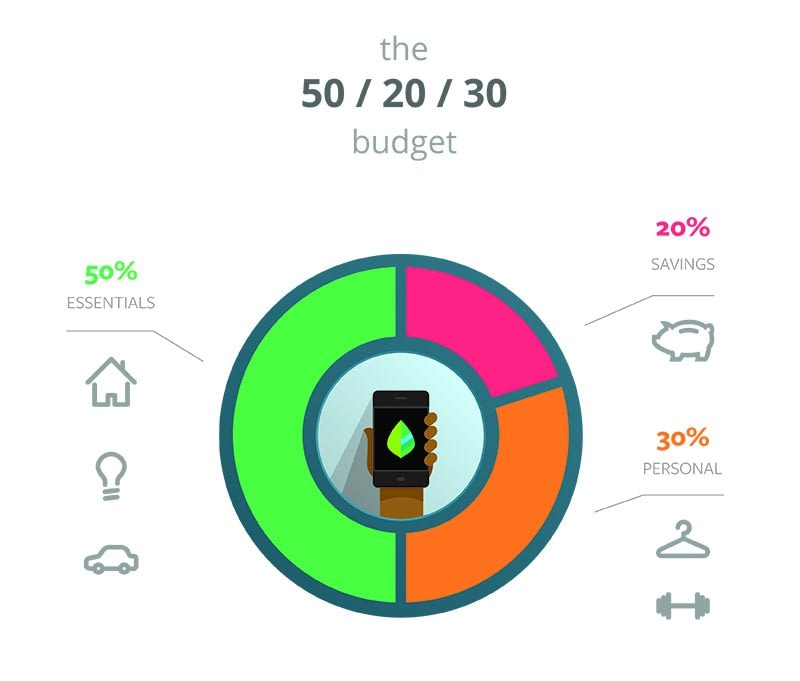

Another concept you can adopt is proportional budgeting, where spending is split up between the essentials, savings and personal expenses. Mint.com recommends a 50/20/30 split: 50% on essentials, 20% on savings, 30% on personal.

This type of budgeting can be an invaluable tool for fresh graduates and those living on their own, though the concept can be adopted and adjusted for anyone.

For both options, organisation and tracking just where your money is going is key to being more frugal with your income, alongside maintaining the required discipline to follow it through.

Emergency Fund

A.k.a. the “rainy day” or the “when you know what hits the fan” fund, this is your emergency reserve for when things go wrong and, in my opinion, the first form of savings you must have in place before any other investments come into the picture.

It is generally accepted that this is about three to six months’ expenses in an easily accessible account. Its purpose is to be there in case of any unexpected event, ranging from job loss, medical emergency, vehicle issues or, particularly for expats, unplanned travel expenses. And I don’t mean an “emergency” weekend away because you think you deserve it.

Of course, everyone’s situation is different. Using the proportional budgeting method, aim to put away 20% of your income to grow your emergency fund. One way to start is as follows: if your expenses total less than 50% of your income, aim for three months; if expenses are more than 50%, aim for six months. The fewer commitments you have, the smaller your fund needs to be.

It is important that your emergency account is liquid — can be taken out in cash easily — so that the safety net is there in times of need. Many people simply keep this amount in their main current account; whilst safe, having these funds as near as your debit card can all too easily lead to frivolous spending (hello new designer shoes!) — not so much an emergency.

Having your emergency fund kept in a separate account stops you spending it on a whim and disciplines you into keeping record of exactly how much you have stashed away. An easy and safe place for this an interest-earnings savings account — simple.

Retirement Planning

Yes, retirement. I know you’re only 28 – but starting early is going to make your wealth grow exponentially towards that pot of money you want for retirement. Have you heard of compound interest? Well, it’s your best friend and works its magic the sooner you start putting away regular monthly contributions. Check out my article on why saving early is essential here.

Whilst you may have a pension scheme through your employer, nowadays it is often not enough to provide for your retirement. Contributing into a personal savings plan as your first step into investing your money is a worthwhile move, especially for those of us living and working abroad where it may be your best option to save up towards your pension pot.

The hardest part is starting…and it hurts. But we must look towards the future and let your money grow on its own accord, which it will.

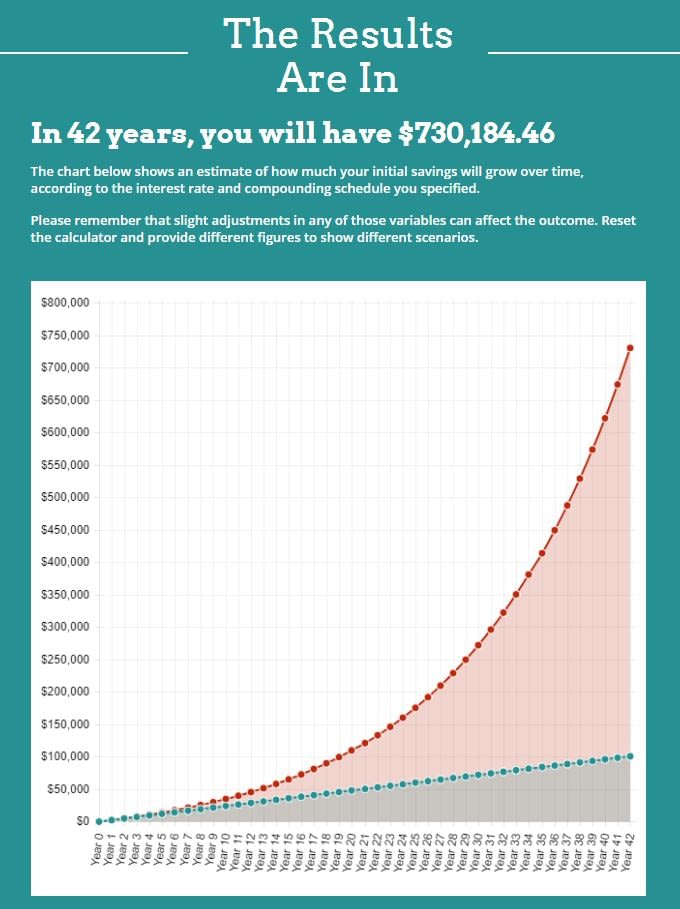

I’ll use myself as a quick example of how a little goes a long way, here using Investor.gov’s compound interest calculator:

Starting at 25 years old, I have no initial investment but decide to start putting away $200 a month up until my retirement, which let’s say is 67, thus 42 years of savings. I estimate an average annual interest rate of 8% — our target average return — on my savings, which is compounded annually. Check out the results in the graph below.

Phoar! Not bad, eh? Here the green line represents the growth without any compound interest, just simply contributing $200 a month over the years. The red line highlights the overwhelming effect of compounding – notice the huge spike in growth as the years go on.

This is also assuming I continue to add $200 each month over the years; it is highly likely that I will increase my contributions as I grow older, so my retirement pot will have grown to even greater heights in the future.

The results are phenomenal – let your money work for itself.

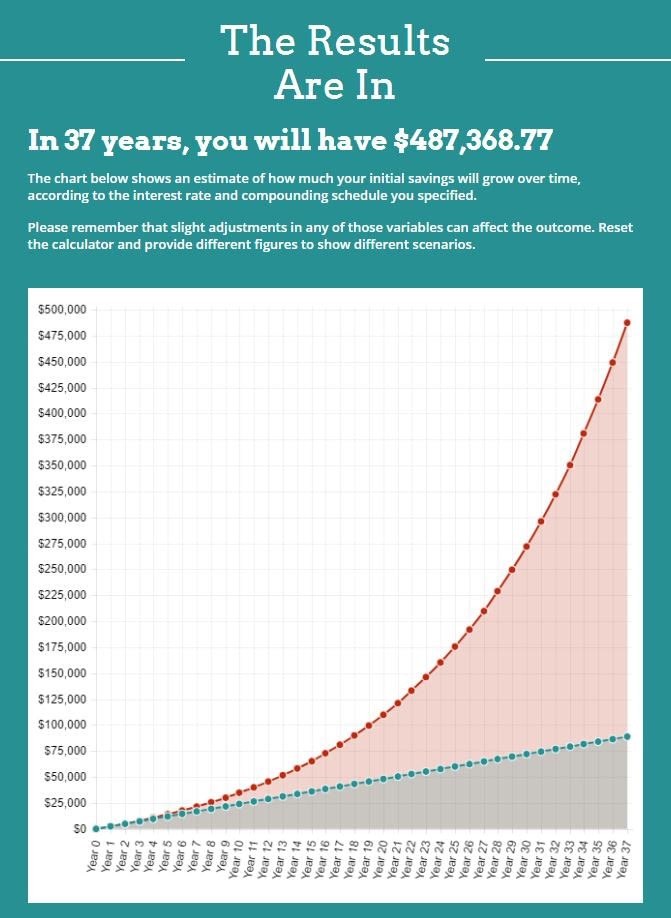

For reference, let’s have a look at the results if I were to begin at 30 years old:

…I’ll leave that with you.

Of course, it is never too late to start saving and reap the benefits of compound interest, but the sooner really is the better.

Have a go yourself with the calculator and see how regular monthly contributions and the magic of compounding can work wonders for your savings.

When you’re done, be sure to get in touch with me at thomas(at)absolutefsl.com to see if a regular savings plan can help meet your financial needs.