Starting your savings plan can be one of the hardest hurdles on your journey to financial health. I get it — you know you should think about it, but that also means actually doing it. But trust me, even if you start small, it really is better than nothing.

If you have already kicked off your savings — well done! If you have been putting it off, making excuses, or prioritising other aspects of your life, maybe 2019 can be the start to your savings, or at least a reorganisation of them. Whether you need to start or have already made way, let’s make it a part of our New Year’s resolution to look at our savings, okay?

Let’s keep this as basic as we can and for the mass, rather than focus on saving for a specific area.

The Mentality

Everyone enjoys a nifty little quote, so how about one of my own? No…? Alright then; here’s some savings advice from a much wiser man than myself, Warren Buffett, coined one of the best investors of all time. You may find him more credible.

This is a great mentality to adopt when considering your savings. Many people put their savings at the end of their financial obligations, waiting for other areas to be addressed first, leaving anything that is then leftover for their savings. This really does have its flaws, even if you might not think so — let’s explore this further.

Scenario 1 — Bob

Take Bob, for example. He gets paid monthly and decides to stash away anything leftover just before his next pay day. He covers any bills, debts and obligations throughout the month, whilst living his day-to-day life and whatever may pop up in between. Bob is, generally, a pretty frugal person who has saved up a few months salary for emergencies and saves a bit each month which he is using towards retirement. Last month, Bob put away $200 — go Bob! This month, however, he could only put away $25 — yikes! What happened?

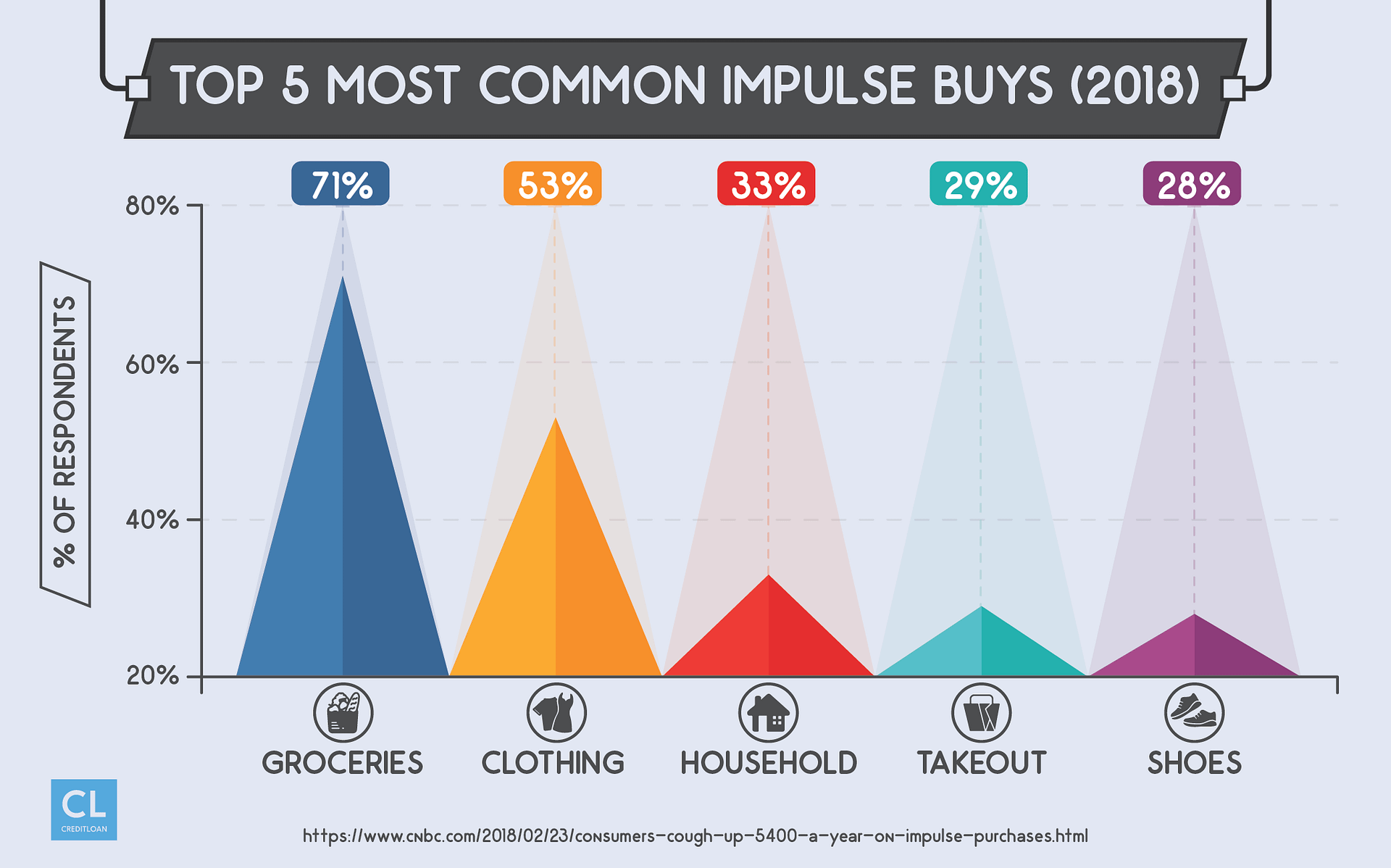

Well, Bob still kept on top of all his bills, any debt etc. and had no major event that resulted in a large payout. However, with the discipline of allocating his savings at the end of the month, he did not have full control of the day-day-day, moreover, any unnecessary expenditure. Buying the top that he’ll probably wear once for that one party; the goose feather pillow that fitted with the feng shui style of his living room, suggested in the overpriced lifestyle magazine he read on his friend’s toilet; the impulse purchase of the subscription to spinning classes that he will definitely get his money’s worth out of. You know what I mean.

Listen now — I’m not suggesting there isn’t place to purchase these “niceties”. I’m a sucker for Netflix, Spotify and I will pay for that decadent, vegan, sweetened with honey, cold-pressed snack…because I loathe processed sugar and I don’t mind spending a tad more of something cleaner for my body. But, I pretty much watch Netflix and listen to Spotify every day (I do have friends) and I only have that type of snack rarely — getting your needs/value’s worth alongside moderation is always key.

However, there is a way to manage both a consistent savings plan and maintain the lifestyle you desire, impulse buys and all, which takes us on to Scenario 2.

Scenario 2 — Bobette

Meet Bobette. Unlike Bob, Bobette puts aside $200 when she gets paid as her first priority. Now, Bobette has planned her finances and knows that this is an amount she can afford to put away, whilst still paying her bills, debts, anticipated day-to-day expenditure; she also has a few months salary stashed away for emergencies. Like Bob, she is frugal and is focusing on saving for retirement at the moment.

At the end of the last month, Bobette set aside her $200 and went about her month. She paid off any bills she could straight away, set aside any bills to be paid midway through the month and broke down her day-to-day expenditure into a weekly amount, focused on fulfilling her basic needs -Bobette likes to organise her finances in advance, as you can tell. With this planned out, Bobette went about her month as usual, armed with an amount of money she knew she had available to spend as she managed her obligations in advance.

Bobette ended up buying that top she had an eye on, decided the pillow really wasn’t a necessary purchase and found out that she got the exercise she wanted from jogging around the park. She even thought ahead, knowing that December would be a more expensive month, what with presents, numerous dinners and New Year’s to plan for, which stopped her buying things she really didn’t need.

Furthermore, Bobette’s mentality allowed her to naturally start saving even more of her funds each month, unlike Bob who, as he had some spare funds available, decided he would buy a whole set of the pillows. Bob thus had a really tight Christmas, not only stressing him out but meaning the holiday season wasn’t as relaxing or fun as Bobette’s.

…yes, of course I am being slightly melodramatic, but I hope you can see the positive knock-on effect of putting your savings aside at the beginning of your month. This method and mentality make it easier to not just save, but also organise your other expenses in relation to what is left.

(Some of you will be glad to know Bob and Bobette will met this Christmas, becoming happily married and financially healthy, with Bob learning a great deal from his new partner. A Christmas miracle indeed!)

The Discipline

So, you’ve got the right mentality; you’re saving first and addressing any financial obligations before anything else, with an emergency fund available that you can rely on if you-know-what hits the fan. Great!

Now, how do you make sure you maintain this discipline? This is where it can be tricky for some; the methods can vary from structured to simply behavioural, so let’s explore a variety of these.

Direct Debit

An easy way to get those funds straight out of your current account and into whatever savings account you have set up. Using automation means you won’t even have time to think about setting the funds aside. There are many savings vehicles you may set up; make sure you know the amount going out of your incoming funds can easily be stored away in your savings.

You can also set up direct debits for debts or bill paying, so that these obligations are taken care of straight away. This can help with budgeting, as seen below.

This reduces the stress of money management and will help you to not even notice the money going out of your account.

Budget

Plan for your month after your savings and major financial obligations have been taken care of first. This will make budgeting for your day-to-day expenditure and knowing how much you have for your leftover “fun” cash heaps easier.

Write out this plan on paper, or use nifty financial apps (like this) to help you plan ahead and manage where you can cut down on any unnecessary expenditure — try your best to stick to it; no one’s perfect.

Remember, this is to help manage your wealth, not completely plan every single move you make — life doesn’t always work out according to plan, but there are ways we can manage and change habits.

Challenges

This may not work for everyone, but try making personal challenges for yourself. This could be small things such as cutting down on Starbucks, making your own lunch or using public transport more. You can make them as serious or as fun as you want, as long as it’s helping you save.

Work out how much you can save by changing small things in your lifestyle — you’ll find out that cutting out a little here and there goes a long way when you add it up at the end of the month. Track these changes so you really can see the savings adding up.

This can be as small as unsubscribing to that retail newsletter you get in your inbox when there’s a sale (when isn’t there a sale?), only buying one coffee per day and drinking more tap water, or resisting the urge to spend on pay day rather than at the end of the month.

Get Support

Set goals with a friend or get financial advice from a friend — maybe they just happen to be an adviser who would happily give you free advice…

Working out a plan with someone is a brilliant way to make sure to you keep on track, as their mentorship will keep you thinking about it and urge you to realise your targets.

At the same time, do your research — savings is a great way to start the journey, but as this grows it is important to make sure you are saving effectively. Professionals are out there to help you manage and grow your wealth in the most effective way for your situation, so seek them out and find out how they can help.

Treat Yourself

At the same time, it is vitally important that whilst you are managing your wealth and putting your savings away, you are also rewarding yourself for reaching your targets and accomplishments.

No, this doesn’t mean splurging your savings on anything unnecessary, but positively acknowledging your achievements from your hard work, which in turn will make it more likely for you to stay on track with your goals.

Maybe you can go and buy that goose-feather pillow for Christmas 2019, after the end of a solid year of saving!

The Implementation

The final step…

Just do it. Get started.

Simple as that, yet often the hardest step to take.

Make this the year you start, or reorganise your current savings goals so that you’re on your way to strong financial health and freedom in the long run.

If I can help, make a plan with me. Drop me an email at thomas@absolutefsl.com for advice, or to meet up for a free consultation if you’re in Kuala Lumpur