Rudolph’s Realistic Returns

Rudolph’s Realistic Returns

Many people know of my beloved reindeer, Rudolph, for his shiny red nose and for leading the way on a cold winter’s night. But what I value most is his calm and collected nature throughout our journey, rather than chasing huge gains on the reins — ho ho ho!

I follow Rudolph’s attitude when it comes to my investments. One of the worst mistakes new or inexperienced investors make is chasing stories they see on the news, the internet, or even their friends who boast double or triple-digit figure returns in the short term. Undoubtedly, this is attractive, but not understanding that these returns are mostly short-lived can cause rash decisions by jumping on the sleigh wagon.

My candy cane takeaway? Keep your target on average annual returns over the years of your investments. Yes, one year’s worth of 30%+ returns is fantastic, whereas a year where your portfolio is less than 5% may hurt — but if over the medium- to long-term your average annual return hits, say, 15%? Milk and cookies all around!

Think of Warren Buffet — whom I taught a thing or two — whose team has achieved an average annual return of 20% since 1965. If you’re hitting near this figure, you’re up there with some of the best in the game.

Frosty’s Cool Head

Ah, Frosty — no one is cooler than he! And this ball of fun does not need a magic hat to know that chasing returns will get him nowhere with his investments.

Flocking to invest when you see large profits in the news, hyped assets by friends, or a surge in company popularity, are easy traps to fall in. Why wouldn’t you want to get the same high returns as others? More often than not, however, you are likely too late to reap the same benefits — think about how many thousands of others are thinking the same as you and jumping into these investments.

Unfortunately, many investors diving in this way will fall short of the high returns these funds achieve due to inappropriate timing when they enter. Often when these funds are hitting the news as they are reaching a maximum threshold and will likely plateau — jumping in now is expensive and may see your returns diminish quicker than you would like. Did you hear about GameStop?

Generally, the steeper something gets, the more likely it will correct itself. Investors in this atmosphere get tempted to trade in the short term and sell at a loss when they do not hit the figures they have seen, falling victim to trying to time the markets — which repeatedly fails for the average investor.

Timing of the Elves

My Elves ensure – without fail – that presents are ready to be delivered on Christmas Eve every year. The secret to their success? Start early. Now, they are not constantly working day in and day out — I do not overwork them! But as they start well in advance of their deadlines, their success is guaranteed, just as it can be for your long-term investments.

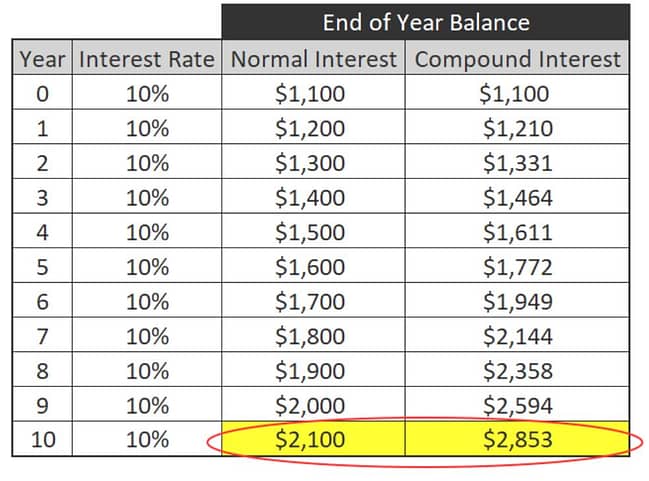

Time is money: the earlier you start, the more you shall be rewarded. You only need to look at the effect of compound interest to see its wonders put to work – it is as magical as me! Compound interest can be defined simply as interest on interest rather than the same interest applied to your original investment. Take a look at this nifty graph below to see what I mean, assuming a starting balance of $1000:

With ‘normal’ interest, you receive 10% of the original $1000 each year, which means you receive an extra $100 each time. However, compounding applies the 10% interest to the previous value, not the principal amount – thus, your interest gain grows with each subsequent turnover.

This can produce massive gains the longer compounding has to take effect as it generates large sums of money to work with, meaning your investment can have a snowball effect the more it grows – and you know I love a good snowball, ho ho!

* * *

Remember, for most of you, your biggest priority is your long-term investment for the future, and it pays to sit back and let it grow, let it grow, let it grow!